Adobe - The Punishment Don't Fit The Crime!

Adobe - The Punishment Don't Fit The Crime!

Adobe/Figma Acquisition - $ADBE $QQQ $NVDA $CRM $TSLA

You have no doubt read of Adobe’s pending $20B acquisition of leading UI/UX “Cloud-Collab” platform Figma - and are likely wondering “what on earth happened to the stock price?”

In brief: the acquisition of Figma will increase Adobe’s TAM from $47B to $63B - $95B*, while securing their moat in the winner-takes-most UI/UX space.

Therefore, as a reward, Mr. Market keelhauled them, shaving a bountiful $47B off their market cap.

Mateys, the punishment don’t fit the crime!

The market’s knee-jerk reaction underscores prevailing "grievance looking for a cause" headwinds, and not any fundamental issues with Adobe, Figma or the (admittedly very rich) deal. Let’s explore why, and also the opportunities this discount may represent for investors.

* (UI/UX TAM estimates reach as high as $50B by end of decade; thanks, in part, to the whopping TAM CAGR of 16%)

First, a brief preamble on the deal

The $20B acquisition will be funded as follows:

• 50% stock - said to be ~7% dilutive, but buy-backs will commence after any term-loan is repaid*

• 50% cash - to hit FCF, and EPS, until earnings are accretive EOY 2025**. The cash tranche may also be partially covered by a loan.

Continuing SBC will also take a bite out of FCF, not EPS, via buy-backs.

* "We will quickly pay down any term loan, if necessary, after close and then resume stock repurchase to reduce Adobe's share count."

** "In year 1 and 2 after closing, the transaction will be dilutive to Adobe's non-GAAP EPS, and we expect it to be breakeven in year 3 and accretive at the end of year 3."

Why Figma? Because..

Figma is a fledgling and intrepid computer-graphics software developer and publisher, penetrating a new multi-billion-dollar TAM at an exponential pace. Remind you of anyone?.. I just described Adobe in the 80’s.

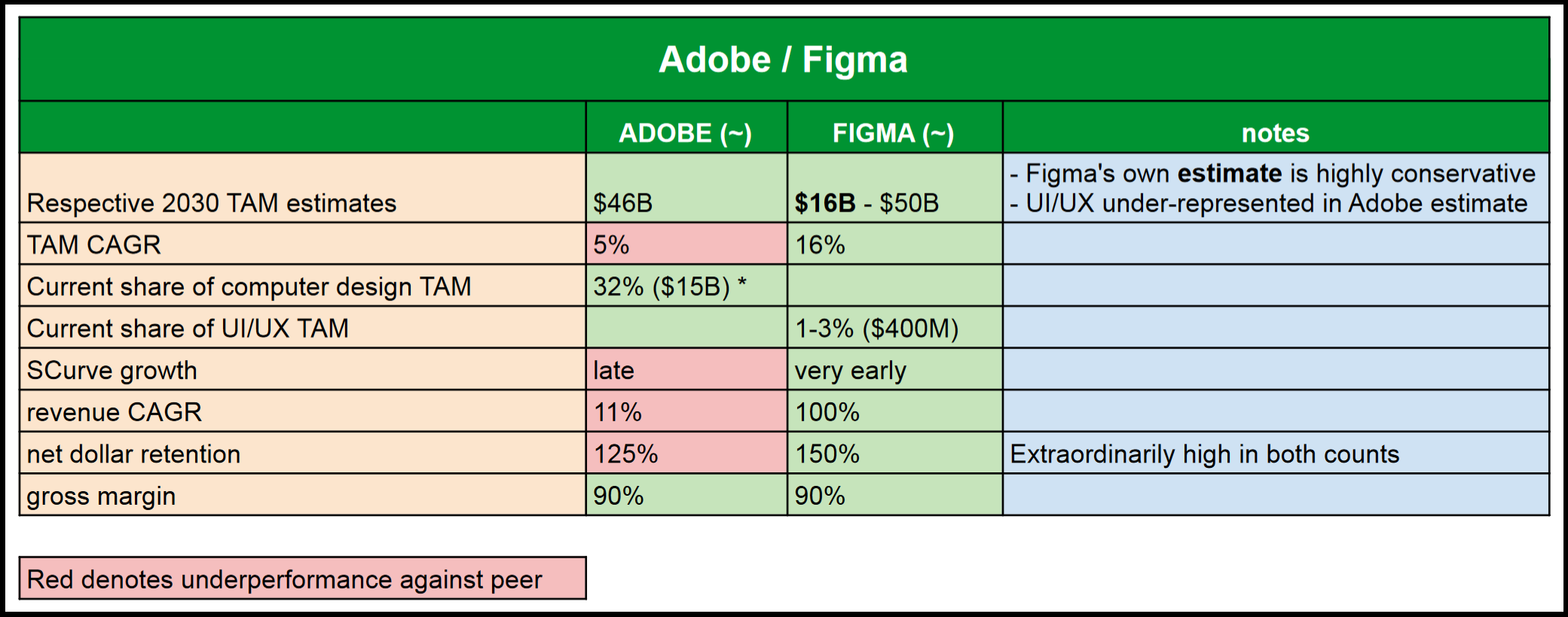

And just look how the two compare even today (see fig. 1 below):

• Both have a gross margin of 90%

• Both have extremely high net-dollar-retention. Adobe 125%. Figma 150%

And I’m sure Adobe has fond memories of its colossal 100% revenue CAGR back in the 90’s. A CAGR enjoyed by Figma today.

Figma’s lead in the Cloud-Collab and UI/UX space is unassailable - just as Adobe’s lead in the computer graphics space in 80’s and 90’s was unassailable. Adobe are worried, and they should be. Figma are eating their lunch. And Adobe just announced this fact through a $20B megaphone.

Now, we know Mr. Market has voted with his money, insisting that “Adobe is wrong”, which begs the question; did Mr. Market suddenly become a UI/UX industry specialist overnight?

• Unlikely

Conversely, is Adobe better equipped to appraise Figma's ability to succeed or fail than Mr. Market?

• Likely

More to come on this, but first..

Let’s examine why the market hates the deal

There is a near endless procession of horrors for the pessimist to gorge themselves upon. Some are valid, some are myopic. Let’s begin with the valid. Here are the lowlights:

Figma is a private business, and private-equity SaaS valuation multiples are much lower than those for public equity; which only worsens the optics on the $20B purchase.

Next is that shareholders were hitherto unaware that Adobe's moat was naked without Figma rounding out their UI/UX offerings. Figma was not perceived to be such an extreme threat until Adobe made their $20B “we are worried!” announcement. The cat is now out of the bag.

The price is also high when compared to Adobe's assets (~$26B) and cash-&-equivalents (~$3.9B). And if Figma cannot sustain their elevated growth rates, or margins, then amortisation will take a huge bite out EPS as earnings will surely fail to be accretive to EPS by EOY 2025, as promised.

Worse still is that the stock tranche of the deal appears to be ~7% dilutive to shareholders*. Adobe already spends ~$1.4B per year to offset their SBC dilution, and must now spend more to offset the dilution caused by the funding of the Figma deal, therefore FCF will be cut by a further ~$1.5B.

* buy-backs will commence after any term loan is repaid

Lastly, this purchase is being made amid the worst consumer-sentiment headwinds seen since the early 80's; putting enormous pricing pressure upon Adobe's stock at the worst possible time.

But Mr. Market’s outlook is myopic

Here are twelve things he missed

Note: from this point onward I will use the mean UI/UX TAM estimate of $33B.

Adobe has eliminated a competitor that was, we now learn, a significant threat to their moat. If they don't buy Figma now they are leaving Figma out there "in the wild" to further steal their market share.

Given Figma's radical pace of growth, and continued market dominance, Adobe have secured their place as leader in the UI/UX market. A new market of which <1.0-1.5% of the TAM has yet been secured.

Figma's business model and products exist within the very centre of Adobe's circle of competence. Therefore the prevailing assumption that Adobe don't understand Figma, and that they have chosen to pay $20B for unsustainable growth rates, is flawed.

Figma have accepted $10B in Adobe stock, so their own tyre-kickers seem to think that Adobe's stock price was attractive at October levels.

Figma are growing into their TAM at an exponential 2x growth pace per year (this is not a typo), providing Adobe with the type of rapid growth that is typically only seen in intrepid, fledgling businesses entering the steep part of their respective S-Curves.

Figma will now be enjoying a swathe of new customers who are either being cross-sold into Figma's offerings, and/or will be gaining new customers who choose Adobe suite-packages that contain Figma's products.

Growing revenue at 100% per year is a lot "easier" for businesses that are early on their growth S-Curve, but, once revenue begins to climb into the billions, it requires large shifts in infrastructure and management to maintain such a growth rate. This is something that Figma has no experience in, while Adobe has 40 years of experience in both.

Figma has a lot of new competition on the horizon, in the likes of: Sketch, Axure, Uizard, Bubble and and a swathe of new companies entering the space. Think Tesla, at the forefront of the EV market with ~20 competitors nipping at their heels. This is where Adobe can help. Adobe's cloud-infrastructure is extremely difficult to disengage from once adopted because businesses don't just adopt one piece of software, but instead a suite of complimentary software - this is why, for example, Davinci's Resolve has not yet usurped Premiere Pro (despite being both excellent and free). Also, those sourcing for design projects want to recruit from the deepest pool of talent available, and that pool is typically comprised of artists familiar with Adobe products. "But is this really working?" - I'd say so, Adobe own 30% of the computer-graphics TAM.

The market appears to have also missed that Adobe is now a cloud-based SaaS infrastructure business first, and a graphics / video program maker second. The quality of their design software must, of course, be excellent; but it is the cloud-collab component that is at the forefront of a paradigm shift within the industry - the component within which Figma is the market leader.

If Figma only penetrates its TAM by ~7.5% by 2025 (which matches the pace of its ARR), and we ballpark the revenue at ~$2.5B; that prices the deal's 2025 PS Ratio at ~8. Now let's put that ratio into perspective against Adobe's own PS Ratio - which looks like this (fig. 5 below):

• 20 under speculative market conditions

• 13 under normal market conditions (mean)

• 8 under devastating (current) market conditions.

Then the deal, against prevailing negative assumptions, appears strong (though admittedly poorly timed).Adobe is now trading for prices last seen in 2019, when they had ~$2.5B of quarterly revenue, despite now having ~$4.4B of quarterly revenue.

If, through Adobe's guidance (borne of deep experience) Figma reach 30% market saturation, just as Adobe have done in their own market, then Figma's revenue could reach as high as $11B, pricing the deal's future PS Ratio at ~2.

Before we get too bullish,

let’s address the elephant in the room:

"Why hasn't Adobe innovated internally?"

Like most megacap tech companies, Adobe's days of organic innovation are fading. Here's an example: at the cost of ~$83M, and by EOY 2019, most of Figma's current software / tools were available (these have of course improved in quality over time, and at additional expense). Yet in the last year alone Adobe has dumped $2.7B into R&D (33x higher than Figma's R&D expenditure) and yet failed to create a compelling new product that can adequately compete with Figma, nor have they adequately improved Adobe XD enough to limit the pace of designers migrating to Figma / FigJam.

There is a forgivable knee-jerk assumption that megacap companies "should be able to" innovate through building teams of intrepid young swashbucklers. But this is extraordinarily rare; they typically become M&A juggernauts instead.

Let's dig into that now..

Big-tech growth strategies have changed

Some ratios to consider (all ranges denote 52wk high to low):

• Adobe (ADBE) fell 61%, to a PS 8.5 and a PE 31

• Salesforce (CRM) fell 55%, to a PS 5.5 and a PE 300**

• NVidia (NVDA) fell 67%, to a PS 11 and a PE 42

• Tesla* (TSLA) fell 52%, to a PS 9 and a PE 66

How can these PE ratios be so high? Especially under such woeful market conditions? And how can a multiples this high be sustained?

Because there is a pattern of large tech companies maintaining their growth, at the expense of bottom-line earnings, through aggressive M&A, S&M, and R&D, (the latter proving more difficult as their ability to innovate wanes as they grow to cumbersome proportions).

It is true that within this market cycle "earnings are now king", so businesses that prioritise revenue and FCF growth over earnings, in an effort to maintain growth and market dominance, are being more than unduly punished.

Despite this punishment, their PE's remain elevated way above the market’s mean; for example the (QQQ) carries a weighted-average PE of 23, while (CRM) carries a PE of 525**, (ADBE) a PE of 34, and (TSLA) a PE of 60.

But why? Innovation through M&A helps these businesses maintain their relevance and their strong growth rates. And investors will bid on these tickers so long as they are seeing adequate growth concomitant with the hit to earnings. I believe Adobe is one of these companies and will hold a higher-than-average PE until there is a macro shift in the way these later-stage growth companies do business.

* Tesla is not listed by Adobe as a peer, for obvious reasons, but I have listed it here to illustrate big-tech ratios

** Up dramatically over October’s ratio

Due diligence and addressing outlier risks

Let’s address some of the possible curve-ball risks that Figma may face:

The incumbents and FTC, who have their foot down on the antitrust gas pedal, may veto the Figma acquisition.

• A nonstarter, as Figma's $400B revenue is unlikely to place them anywhere near the top of the list for an antitrust investigation.

Being private, Figma's accounts can not yet be independently verified.

• This requires that investors put on their speculator's caps and ask themselves if either Figma, or Adobe, have a history of impropriety. The answer is “no”.That Adobe may retire Figma.

• I highly doubt this, and with good reason: employee retention ought to be strong as the ~6M RSUs (being given to Figma's ~800 person workforce) have a four year vesting period (based on milestones & tenure duration) which will give Figma personnel a strong incentive to continue their hard work and to stick with the company through at least EOY 2026.

• Therefore Adobe cannot liquidate Figma without causing an unrecoverable landslide of ill-will, they would be finished. This would also destroy Adobe's already tenuous relationship with Microsoft.

• They would also be back to fending for themselves using their in-house (and inadequate *) Adobe XD, against a swathe of new Figma clones.

* a legacy desktop design tool for which there is falling demand as the market now favours Figma's tools and their web-based approach.

Putting it all together

I hope I have adequately conveyed that:

Adobe just bought pole-position in the UI/UX market.

Adobe’s method of growth through M&A is typical for a megacap giant.

Figma’s lead is unassailable.

This is an opportunity to own Figma at the beginning of its $33B TAM S-Curve.

Under Adobe's watchful and experienced eye, Figma are likely to be given the tools necessary to grow, at scale, into their UI/UX $16B-$50B TAM.

The “expensive” deal's revenue multiple is in free-fall, and the deal’s price/revenue ratio could hit as low as ~8 by 2025.

Based on sales, FCF, and book value, investors are being offered Adobe at prices seen a decade ago.

Adobe’s tyre-kickers have very likely done a better job at valuing the deal than Mr. Market ever could.

Figma need Adobe (growing into billions of revenue, and building sticky market share against new competition) as much as Adobe need Figma (can’t beat ‘em buy ‘em).

Conclusion and looking forward

The opportunity:

The dollar has been frothy for ~3 months, but equities and bonds, though up recently, are not up 1:1 with the dollar’s fall. This suggests, to me, that equities have been bid on slowly, without waking up prices too much, therefore the recent pullback may not be as extended as the crowd is anticipating.

Exuberance in T-Yields is also showing signs of slowing. And the bond market has been calling most of the shots for the Fed. So we may be seeing the pace of rate hikes rolling to a stop over the next couple of quarters. This typically coincides with improved equity and bond market conditions.

The risks:

If Figma fail to maintain their competitive advantage and excellent growth rate then Adobe is in big trouble, as the deal’s multiple will become too rich to digest.

There is also the macro risk that the recent fall in CPI was an anomaly, and that inflation continues higher*, causing T-Yields and the USD to renew their ascents, and for multiples to renew their compression.

A strong dollar also hurts Adobe’s sales, which are booked in USD.

* This can be caused by: escalating strife in Russia/Ukraine, pushing up oil and fertiliser costs - further supply chain disruptions in China, pushing up costs for goods and some commodities - overzealous fiscal policy, incentivising consumer discretionary spending - another commodities boom, pushing up prices for everything - the list goes on. This, in my opinion, is no time to “buy, hold and forget”.

My own position and strategy

* I can demonstrate that I posted this trade idea elsewhere on OCT5 2022.

You can DM me with a request should you wish to see it *

• In early OCT22 I shorted the JAN23 $290 strikes for ~$27

• IV was ~45

• IV rank was ~78

• The JAN23 expected move was +/- 14%

• Break even was ~$257

• ROI was capped at ~$27

• Adobe rallied, and at ~$300+ I closed out the short puts for ~$20 and rolled the profits (and some fresh capital) into ADBE commons

• I am holding, for now

• If volatility expands again, if the dollar shows renewed strength, or if T-Yields renew their ascent: I will sell the entire equity position until we see signs of calmer seas.

Disclosure

I have no business relationship with Adobe.

I have a long position in Adobe commons.

This article expresses only my opinions and actions. It does not constitute investment advice. I take no responsibility for your investment decisions.